The Reckoning

The Acquisition Reckoning: A Two-Part Series

This is the second in a two-part series on The Acquisition Reckoning.

Read Part 1: The 20-Year Machine.

Something structural shifted in the defense industrial base over the last decade, and it didn’t wait for the acquisition system to catch up.

Venture capital found defense. Companies like Anduril, Palantir, Shield AI, and Saronic raised billions in private capital, built working systems, and showed up to compete for government contracts with mature technology rather than paper proposals. SpaceX demonstrated that a commercial company investing its own capital could outperform cost-plus incumbents on cost, schedule, and technical ambition repeatedly. The drone industry, largely built on commercial supply chains and private investment, are producing more battlefield-relevant capability in five years than the traditional acquisition system delivered in two decades of UAS development.

It happened because the technology environment changed, private capital chased the opportunity, and an initial wave of enterprise reforms in rapid (MTA) and software acquisition, along with contracting (CSOs and OTs). These created enough of a crack in the wall for non-traditional companies to get a foothold. The question now is whether the institution reshapes itself around what’s working, or continues treating these as exceptions to a system that remains fundamentally unchanged.

A different model is taking shape. Here’s what it looks like.

The Funding Inversion

The sharpest structural difference between the legacy model and the emerging one isn’t contracting vehicles or program structures. It’s who funds development, and what that means for how companies behave.

Traditional primes invest roughly 3-5% of revenue in R&D, most of it recovered through indirect cost reimbursement. The government funds the input; the prime uses it to compete for the next contract. Financial exposure is limited. The incentive to move fast is limited accordingly.

Non-traditional, venture-backed defense companies operate on an entirely different logic. They raise private capital from VCs and PE firms expecting commercial returns and burn it to develop prototypes, build products, and demonstrate capability. R&D investment runs 10-20% of revenue, privately funded, with no government reimbursement backstop. They operate with negative net income for years. The business model only works if they eventually win production contracts at scale.

When a company is spending its own capital to develop capability, it has every incentive to move fast, stay close to the operator, and build something that actually works in the field. When a company is spending government money on cost-plus development, the incentives run the other direction. More staff, more time, more process which increase allowable costs and contract value along with the margins.

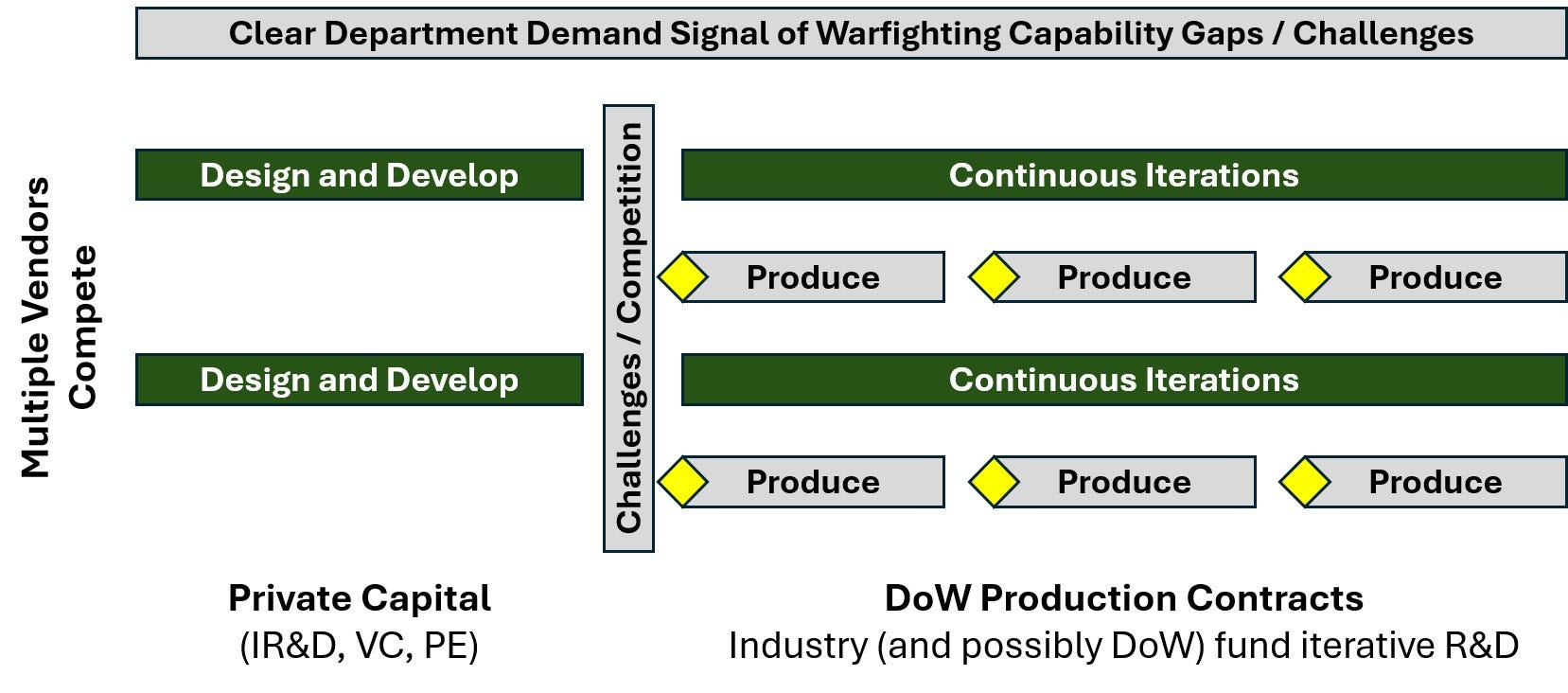

The emerging model is built on the premise that the government should compete for the output of industry’s private investment, not fund the input. Define the capability gap. Let industry invest in solutions. Then run a competition for production. The graphic below shows what that looks like in practice: private capital funds development on the left, a challenge or competition narrows to winners in the middle, and recurring fixed-price production contracts drive iterative delivery on the right.

Large production contracts are the ultimate signal to industry to invest and compete.

Operational Needs Over Specification Sheets

The requirements system in the legacy model starts with a detailed specification. Here is exactly what the system must do, how it must perform, what interfaces it must support, what environments it must survive. Industry responds to that specification. The government evaluates conformance to it. The result is a procurement process optimized for compliance rather than capability.

The new model inverts this. Rather than specifying a system, DoD articulates an operational need and a capability gap. For example:

Neutralize small UAS threats in a contested urban environment.

Provide persistent ISR coverage across a distributed maritime theater.

Industry then brings solutions. Acquirers, testers, and operators evaluate them in realistic conditions through exercises, experiments, and demonstrations. The government selects based on performance, not paper.

Capability gap statements create space for industry to bring whatever solution is most effective including solutions the government didn’t know to ask for.

With JCIDS disestablished, the Services have a genuine opening to rebuild their requirements processes around rapid, iterative, digital mission engineering. That opening won’t stay open indefinitely. The Services that move fast to replace JCIDS with something genuinely different will be positioned to take advantage of the new model. The ones that recreate JCIDS under a different name will not. As Bill Greenwalt and Dan Patt wrote in their Required to Fail report:

“JCIDS is beyond redemption. The only responsible course is to put it out of its misery, carve it from the DoD’s body, bury it, and salt the ground so that nothing resembling it ever grows back. Now is the time for courage, not to fix JCIDS but to kill it.”

The Core Mechanics

The emerging model has several interlocking features that, taken together, represent a genuine structural departure from the legacy approach.

Fixed-price production competitions on recurring cycles. The new model centers on recurring competitions for fixed-price production contracts every few years, across a PAE portfolio. The incentive to innovate continuously is built in. Awarding to multiple vendors where feasible sustains competition and industrial base depth.

Portfolios over programs. The Portfolio Acquisition Executives (PAEs) manage suites of capabilities across multiple vendors. A counter-UAS portfolio executive manages sensors, effectors, C2, and logistics as an integrated capability set, not as four separate programs each running its own acquisition. This enables cross-domain trades, faster technology insertion, and a purchasing posture that looks more like a commercial enterprise managing a product portfolio.

Modular Open Systems Approach (MOSA). MOSA is the technical enabler of continuous competition. When systems are built on open architectures with common interfaces and published standards, mid-tier suppliers can compete to provide subsystems and upgrades without going through the prime. Markets form at the component level. Technology refreshes faster and more cheaply.

Commercial-first contracting. Commercial is the default; explicit justification is required for anything else. This starts at how requirements are defined and acquisition strategies are built, not later when exploring contracting vehicles. The FAR was designed for a shrinking share of what DoD needs. Contracting leaders within each portfolio must rethink contracting norms.

Where Things Stand

The Acquisition Transformation Strategy, a wave of executive orders, and several years of NDAA provisions have put real reforms on the table. The people pushing these changes are serious, and the political will behind them is genuine.

But reform momentum and structural change are not the same thing. The acquisition system has absorbed reform efforts before. The Goldwater-Nichols era, the Packard Commission, the Better Buying Power initiatives all failed to drive lasting change because the underlying incentive structures, budget processes, and workforce habits that produce the legacy model remained intact.

The ATS has 38 initiatives, each with subordinate actions. The SECWAR’s memo added 11 priority actions. The biggest risk to their success is the limited bandwidth of key staff and leadership to execute transformational reforms on top of an already demanding day job. The DoD should resource small, high-performing teams to drive a focused set of priority initiatives to completion and only then move to the next set.

What’s moving: PAEs are the most visible and promising transformation. The Army moved quickly, pivoting all PEOs to PAEs with Capability Portfolio Executives managing sub-portfolios. The Navy, Air Force, and Space Force followed with phased implementation. PAEs are the linchpins of the new Warfighting Acquisition System. Much work lies ahead in deconstructing program barriers into dynamic portfolios which requires dynamic requirements and budget systems but the foundation exists.

What Needs a Surge

“Structure programs as schedule-driven capability increments with aggressive production delivery schedules, unit-cost ceiling goals, and broad mission effectiveness goals. Make trade-offs throughout the development to permit iterative enhancement and rapid delivery of subsequent increments. Make prudent cost, schedule, and performance trades that prioritize time-to-field, including execution of portfolio-level programming within defined and authorized boundaries.”

Agreements officer capacity. OTA authority without a trained agreements officer workforce is an unfunded mandate. The population of practitioners who can structure, negotiate, and administer OTA agreements at the pace and volume the new model requires is too small. DoD lost thousands of contracting officers over the last year, compounding the problem as contract actions rapidly scale. The shortfall of agreements and contracting officers will be the number one bottleneck for regrowing the industrial base and executing a potential $1.5T FY27 budget. Fixing it requires a deliberate workforce development campaign.

PPBE reform. Some flexibility has been gained. But the program-centric budget structure still dominates in practice, and the two-to-three year funding on-ramp that prevents rapid response to emerging capability needs remains largely intact. Portfolio-level funding flexibility is the ability to shift funding within a PAE portfolio without approval of all four Congressional committees is a priority. This requires rebuilding trust and expanding collaboration between DoD executives and Congressional appropriators. The RDT&E-to-procurement ratio, still heavily weighted toward government-managed development, needs to shift substantially to fund production of commercially developed capabilities at meaningful scale.

Test infrastructure. The Department cannot run recurring competitions, rapid prototyping, and operator-driven evaluations without the test ranges, experimentation environments, and digital sandboxes to support them. Industry cannot demonstrate mature capability if there’s nowhere to demonstrate it. Test infrastructure investment has lagged the reform agenda and needs to catch up. It doesn’t generate headlines, but it determines whether the new model works in practice.

Demand signals at scale. Non-traditional companies invest private capital based on their assessment of whether a viable market exists. Multi-year procurement commitments, predictable competition cycles, and clear capacity targets give them the market signal they need to justify continued investment. Without those signals, the rational choice for a VC-backed company is to limit defense exposure and chase commercial markets with more predictable returns. Closing that gap requires procurement commitments that function as genuine demand signals, not rhetoric.

Production competition by design. The current reform agenda has expanded the front end of the acquisition lifecycle with more pathways, prototyping, and experimentation. Recurring fixed-price production competitions built into the program structure from the outset, with defined cycles and published criteria are not yet standard practice. They should be the default for capability areas where multiple vendors can compete. Drive more partnerships between traditional and non-traditional defense companies as well as the emerging flexible production enterprises.

Continuous improvement is better than delayed perfection.

-Mark Twain

What It Takes From Each Player

The new model doesn’t materialize from strategy documents and executive orders. It requires specific behavior changes from specific actors.

Congress has to fund capability portfolios, not just programs. Multi-year procurement commitments including new, low-cost capabilities function as real demand signals. Authorization and appropriations postures that enable portfolio-level budget flexibility. Restraint with fewer program-specific earmarks and fewer oversight requirements that add process without adding accountability where it matters.

OSW and the Services have to build the infrastructure the new model runs on: PAEs with real authority, test ranges, experimentation environments, requirements processes that produce capability gap statements rather than specs, and feedback loops that give Combatant Commanders a direct line into acquisition priorities. The Services that move first and move boldly will shape what the new normal looks like.

The acquisition workforce has to develop genuine fluency in the tools now available, commercial and fixed price default preferences, and iterative requirements development. That requires training, but more than training it requires a career environment where using these tools is rewarded rather than penalized. Acquisition professionals who take risk on new contracting approaches and succeed need to see that reflected in their careers. The ones who default to FAR and deliver slow outcomes need to see that reflected too.

Traditional primes have the most structural adaptation to do, and the most to gain from doing it well. These are companies that organized themselves rationally around the legacy incentive structure and the structure is changing. The companies that invest their own capital in competitive capabilities, embrace MOSA even when it costs them integration revenue, and build genuine partnerships with faster-moving start-ups will grow their share of an expanding defense budget. The ones that defend the legacy model past its useful life will find their market shrinking as portfolio executives direct spending toward vendors that perform.

Non-traditional companies have to close the production gap. Winning a prototype OTA is only the beginning. Speed is a competitive advantage until it isn’t. Execution at scale is what sustains a defense business. This is why we’re seeing massive funding rounds and new partnerships by the largest War Unicorns.

The Window

The acquisition system has a long institutional memory and strong reversion tendencies. Reform efforts that don’t change the underlying incentive structures including how budgets are built, how contracts are structured, how careers are made eventually get absorbed. The system doesn’t resist change through malice. It resists through the accumulated weight of process, precedent, and rational individual behavior under existing incentives.

What’s different this time is the convergence of factors that historically haven’t aligned: genuine political will at the top of the Department, a commercial defense sector mature enough to compete for major programs, a threat environment that makes the cost of delay visible and concrete, and a body of legislative reform substantial enough to support structural change if the institution chooses to use it.

The window is open. It has been open before and closed without the change taking hold. Whether it closes again depends on whether Congress, acquisition executives, and the industrial base treat this moment as the beginning of structural transformation or the latest season of reform theater.

The capability exists. The authority largely exists. The question, is will.

Join over 16,000 defense and industry subscribers to get our weekly recaps and thought pieces. Paid subscribers also get budget and legislative analysis and are valued supporters of our work.

While I agree with everything written here -- as with so much of the discussion over the past 30 years it's what is missing that is telling. All the fixes are focused on Acquisition, but the underlying problem that has been repeatedly identified is with the Requirements -- and there is absolutely no mention of the Requirements (or Capability) Development workforce or activities. It's all well and good to mention rather simplistic capabilities like "[n]eutralize small UAS threats in a contested urban environment" or "[p]rovide persistent ISR coverage across a distributed maritime theater," but WHO generates those phrases, and what is a comparable description for large scale ground combat?

We MUST have Capability Developers (particularly in the Army it seems, as the other services seem very focused on countering platforms vice formations) who can look at enemy capabilities at both the system and formation level and articulate how to defeat formations by defeating/degrading systems. As an example, there remains a tendency to believe that the only way to defeat a Main Battle Tank (MBT) is to defeat it by kinetic means, hence the continued growth in both calibers and kinetic capability -- rather than looking at what happens when fire control or electronics are compromised.

But absent a conscious decision by leadership to train and educate the workforce, AND provide the analytical capabilities (simulations) to rapidly assess various capabilities at the system and formation level, this part of the equation will never change, and we will not achieve the paradigm-shifting change at scale necessary. Almost every positive example thus far has been relatively small-scale in the context of the entirety of the services' capabilities -- and has been the result of very focused leadership, which is not scalable service-wide.

I am glad that we are fixing the manufacturing and delivery parts of car business, but we need to be fixing the design piece as well so we can stop with the Edsels and move forward with the Mustangs.

I strongly subscribe to the adage that “every system is perfectly designed to get the results it gets.” It forces me to question what happens 5–10 years down the line: how R&D is sustained and how resilient supply chain sourcing is achieved under the operational‑capabilities, firm‑fixed‑price approach.

When today’s defense startups reach the point where their early investors need to get their money out—through a sale or a stock market listing—what is the dominant path?

If they stay private longer, how do they finance the level of R&D this model assumes once the early funding rounds are behind them, especially when their total available market is effectively the U.S./allied governments, and serviceable available market is those minus allies that won’t touch ITAR?

For all the talk of “dual use,” in practice, export controls close off large parts of the global market very quickly. If ITAR applies, the product is often dead on arrival for much of Europe. That makes the “invest ahead, recoup in volume across many buyers” ethos much harder, even in a production‑first world.

If they do go public, will they remain R&D‑heavy companies at the expense of lower short term earnings? Public investors scrutinize gross margin, and the fastest way to improve it is to reduce Cost of Goods Sold, enabled by sourcing cheaper inputs.

In the absence of sourcing restrictions and few exist today, the lowest‑cost inputs will always come from government subsidized, non-market economy, Chinese owned firms or non-Chinese firms producing in China, a problem that applies to the traditional and non-traditional alike regardless of contracting mechanism.

What happens if most of these firms get acquired by traditional defense players? There will always be a need for exquisite systems, and the traditional primes’ risk‑averse culture and specialization give them structural advantages there.

Do we end up with a bifurcated ecosystem where traditional primes remain the suppliers of exquisite, slow‑cycle systems and a handful of attritable, faster‑cycle systems?

Or can primes adapt to this production‑first, portfolio‑centric model instead of just absorbing startups back into the status quo operating system?

These questions tie directly into the firm‑fixed‑price and operational‑capabilities question. Firm‑fixed‑price feels aligned with attritable systems with shorter development timelines where iteration in production is the point.

But does FFP work for exquisite systems with long, low-risk tolerance development cycles, especially when regulatory constraints prevent firms from spreading that risk over a broad export customer base?

If a company can’t amortize its R&D or capex over many buyers, the unit prices under FFP either have to be very high or something has to give—R&D spend, supply chain resilience, or both.

If we want resilience, security, reliability, and safety, defense will always be higher cost than commercial.

If programs meet their schedule or deliver early, and stay at or under budget, or not far over budget (recognizing sometimes there are unforeseen supply chain shocks and events that significantly increase costs), where “cheaper” is a matter of relative to the status quo, progress has been achieved. Is that an outcome we are willing to accept so long as capabilities that improve outcomes are fielded?

I question how much OTAs and portfolios can shape incentives, especially given potential overlap or duplication of efforts given coordination challenges between the services, combatant commands, and OSW though there have some recent bright spots in terms of one service leveraging another’s solution.

If OTAs at scale become another way to backfill IRAD, we haven’t inverted the funding model. But the most fundamental question long term is can the funding model be inverted in the defense market?

Is there a realistic path where OTAs, PAEs, and capability portfolios consistently lead to recurring fixed‑price production competitions at scale, rather than prototype purgatory—and where they explicitly account for the fact that many vendors cannot freely cross‑subsidize from non‑DoW customers because of export controls?

All of this feels tightly coupled to the underlying demand signal, the contract mix, and financing.

Without broad, authorized and appropriated, normalized use of multi‑year procurement and true portfolio‑level funding flexibility, which the Department cannot implement by itself; deliberate contract designs that distinguish where FFP makes sense (attritable, modular, multi‑buyer) versus where cost‑type or hybrid models are still necessary (exquisite, heavily export control-constrained); and changes to appropriations/budget and tax laws that restore R&D immediate expensing so long‑term R&D isn’t structurally disfavored, the rational choice for most investors will be to take a few defense wins and then pivot back to commercial markets where the return profile and customer set are more predictable.

The technology may be here, some but not all authorities exist. Unless we solve the R&D financing problem under real‑world regulatory constraints, and supply chain policies, the underlying economics may struggle to support and sustain a resilient and reliable production‑first model.

A few questions:

- How is sustained R&D financed for firms operating under FFP and capability‑gap competitions when export controls limit their ability to sell beyond the USG?

- Where would you draw the line on FFP versus cost‑type contracts once you factor in export controls and single‑customer dynamics?