Keeping Score on Procurement Reform

Data indicates reforms have stalled. FY26 is the real test if this time is different.

Over the last year, the Trump administration has prioritized procurement reform, and specifically, the acquisition of commercial products. In Secretary of War Pete Hegseth’s “Wartime Footing” speech last year, he boldly stated “We will prioritize the purchase of industry-driven solutions, commercial solutions first, that meet our needs faster, even if that means bids do not meet every requirement.” The rhetoric mirrors Section 1822 of the 2026 National Defense Authorization Act (NDAA), which essentially requires the Secretary of War to approve every noncommercial acquisition. There is also Executive Order 14271 from April 2025, which requires every agency to review ongoing acquisitions that should have been commercial but were not, and Executive Order 14402 from April 2026, which mandates fixed-price contracts as the default.

These actions were welcome news for those of us who have long appreciated the straight line from effective procurement to a lethal warfighting force. The defense industry’s divergence from the commercial economy has led to unnecessary requirements and billions in waste while extending major program acquisition timelines to well over a decade—or two. Defense reformers have been burned in the past by failed attempts to encourage commercial acquisitions, but the strength of these initiatives leads many to believe that this time will be different.

Fiscal Year (FY) 2026 is the first full fiscal year under the new administration. It marks an inflection point: either we see the reforms begin to bear fruit, or FY 2026 looks much like the years before it. My new analysis of the Department of War’s spending from FY 2012 through FY 2025 shows that, based on the available data, little meaningful progress has been made in acquiring commercial solutions, buying products from commercial companies, or diversifying away from the five prime contractors. The data instead provides evidence of the acquisition workforce’s and legacy contractors’ enduring resistance to change. Breaking the bureaucratic status quo will require sustained and meaningful action.

The More Things Change

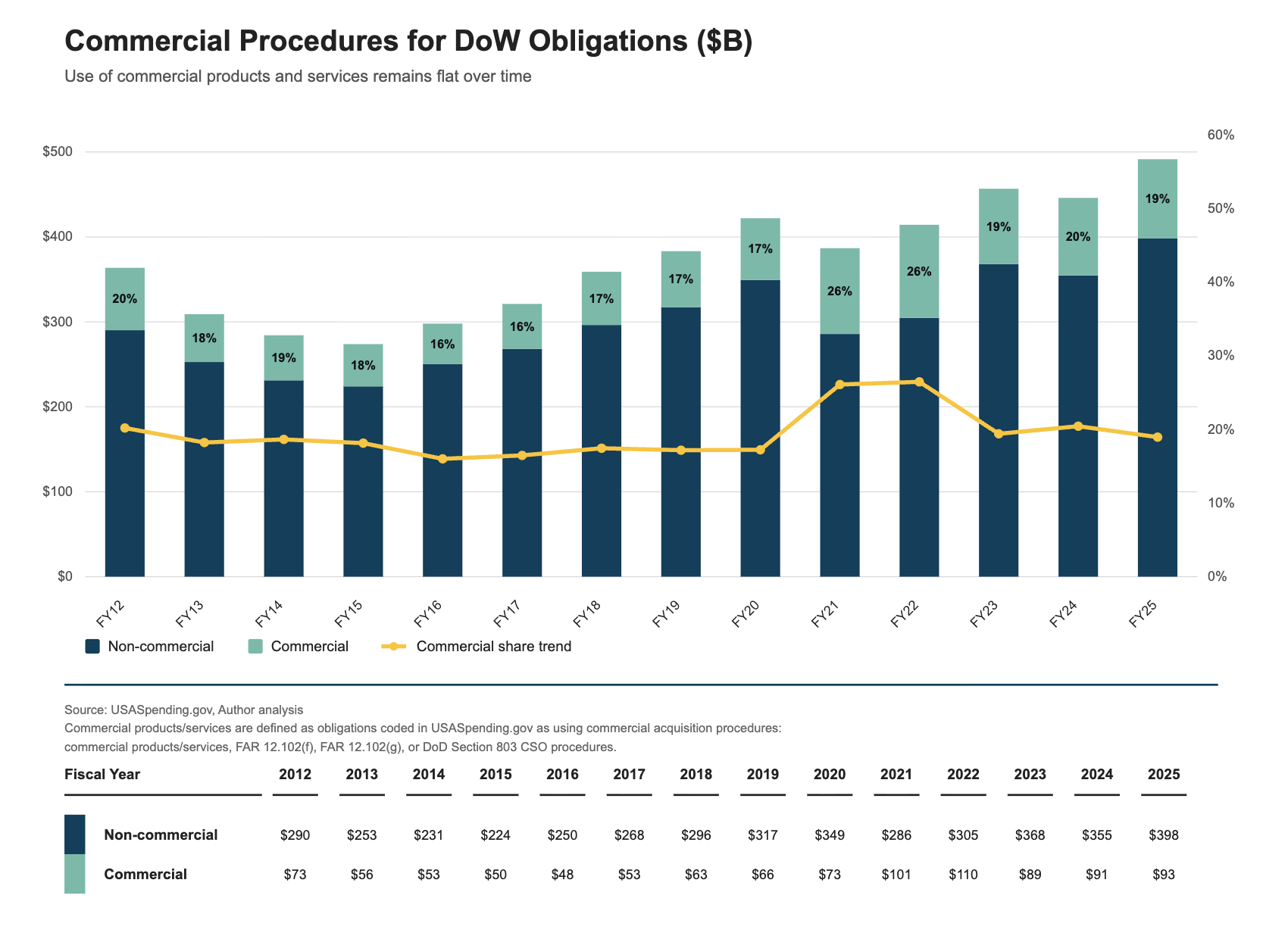

The share of defense spending on commercial technology is no higher today than it was 14 years ago—a staggering fact when one considers the hundreds of billions of venture capital dollars invested in U.S. defense tech companies in the last six years. The government is required to buy commercial technology to the maximum extent practicable per the Federal Acquisition Streamlining Act (FASA) of 1994. Such products are developed at private expense and sold to the government via fixed price contracts. The logic is that industry eats the risk but also captures financial upside if its products are successful. Despite the law, the share of spend on commercial technology since 2012 has fluctuated between just 16 and 20 percent (save for 2021 and 2022, when pharmaceutical purchases during Covid led to outlier commercial spending).

The nadir of the relationship between defense and industry was 2016, when the Department of War spent just 16 percent on commercial technology. 2016 was also the year Palantir first sued the government over FASA violations—and won. If you squint, there has been some progress in procurement since then. Fiscal years 2023 to 2025 were better for commercial technology than 2016 to 2020, but only by a couple of percentage points. Even this meager progress has plateaued at around 19 percent. When the private sector outspends the government on research and development by four to one, it beggars belief that over 80 percent of defense solutions can only be built with non-commercial technology.

There’s an argument to be made that the percent spent on commercial technology is undercounted when the criteria is limited to FAR Part 12 (i.e. FASA). DoW has interpreted FASA’s “commercial item” and “of a type” provisions narrowly, limiting commercial treatment mostly to goods that already have an established commercial market—even though the statute’s language was designed to reach further, up through fully bespoke development using commercial practices. As a result, products that are privately funded and priced commercially but lack an existing commercial market do not get characterized in the data (or in preferential treatment) as commercial. AEI’s William Greenwalt proposes a different fix: rather than trying to define what counts as a commercial item, he would have DoW treat all non-traditional defense contractors (NTDC) as commercial entities, determining commerciality at the business-unit level instead of contract by contract. Another option is to establish a standardized rubric for determining commerciality that KOs can easily use.

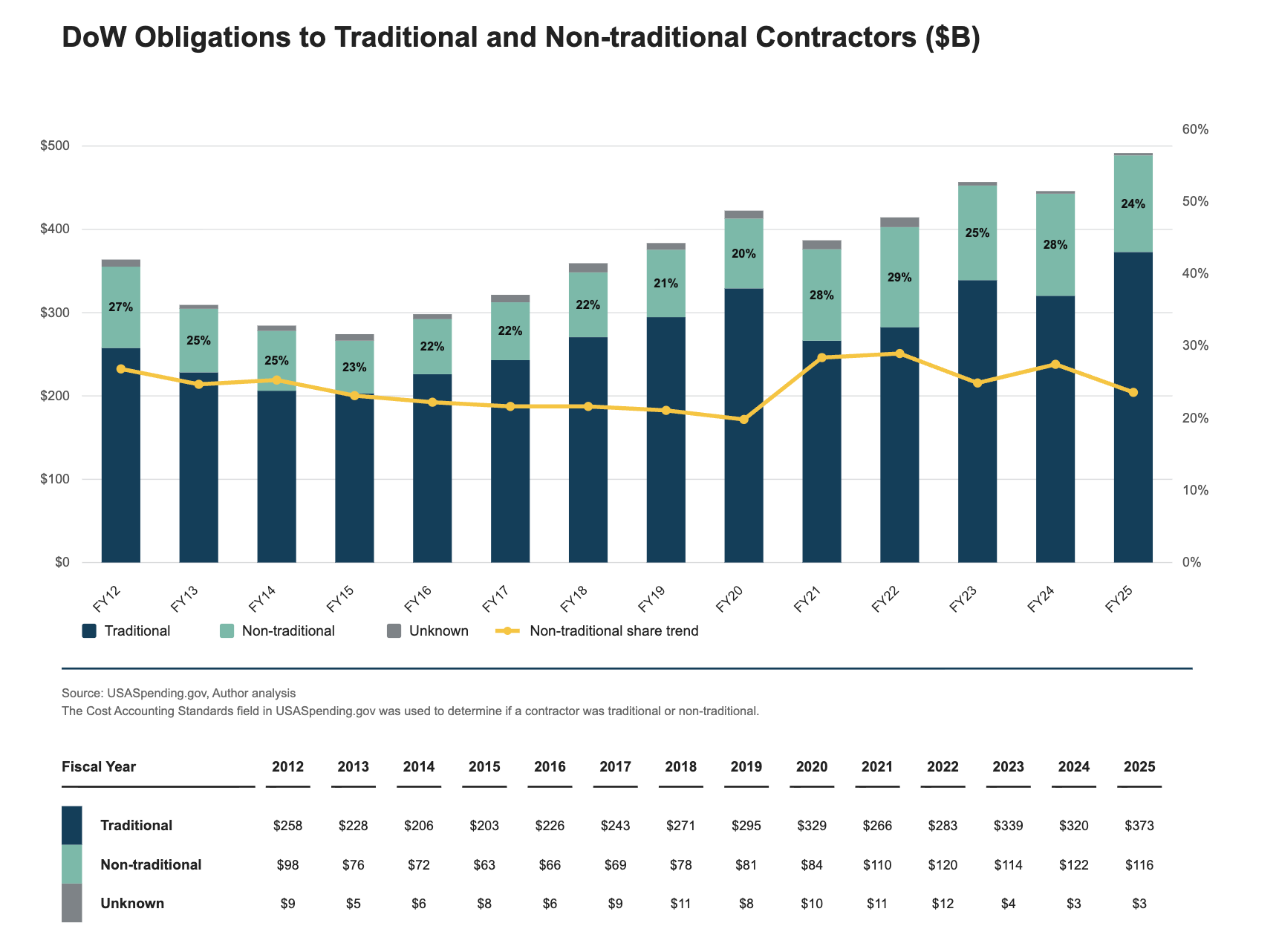

A second meaningful data point is the share of obligations earned by NTDCs. An NTDC is any company that, within the last year, has not performed a contract or subcontract subject to the full Cost Accounting Standards. This broad definition applies to over 90 percent of contractors and includes commercial companies, yet NTDCs receive only about 25 percent of dollars.

About half of NTDC awards are not counted as commercial. If commerciality were determined at the entity level rather than the contract level, the percent of spend on commercial would rise by an additional 12 to 13 percent. This would increase the commercial number to about 30 percent—still too low, but a meaningful improvement.

Like with commercial contracts, the share of spending that goes to NTDCs has not noticeably improved over time. It’s possible that companies with a business model geared for the normal, commercial economy either cannot effectively compete for defense contracts or have chosen not to. Neither option is good.

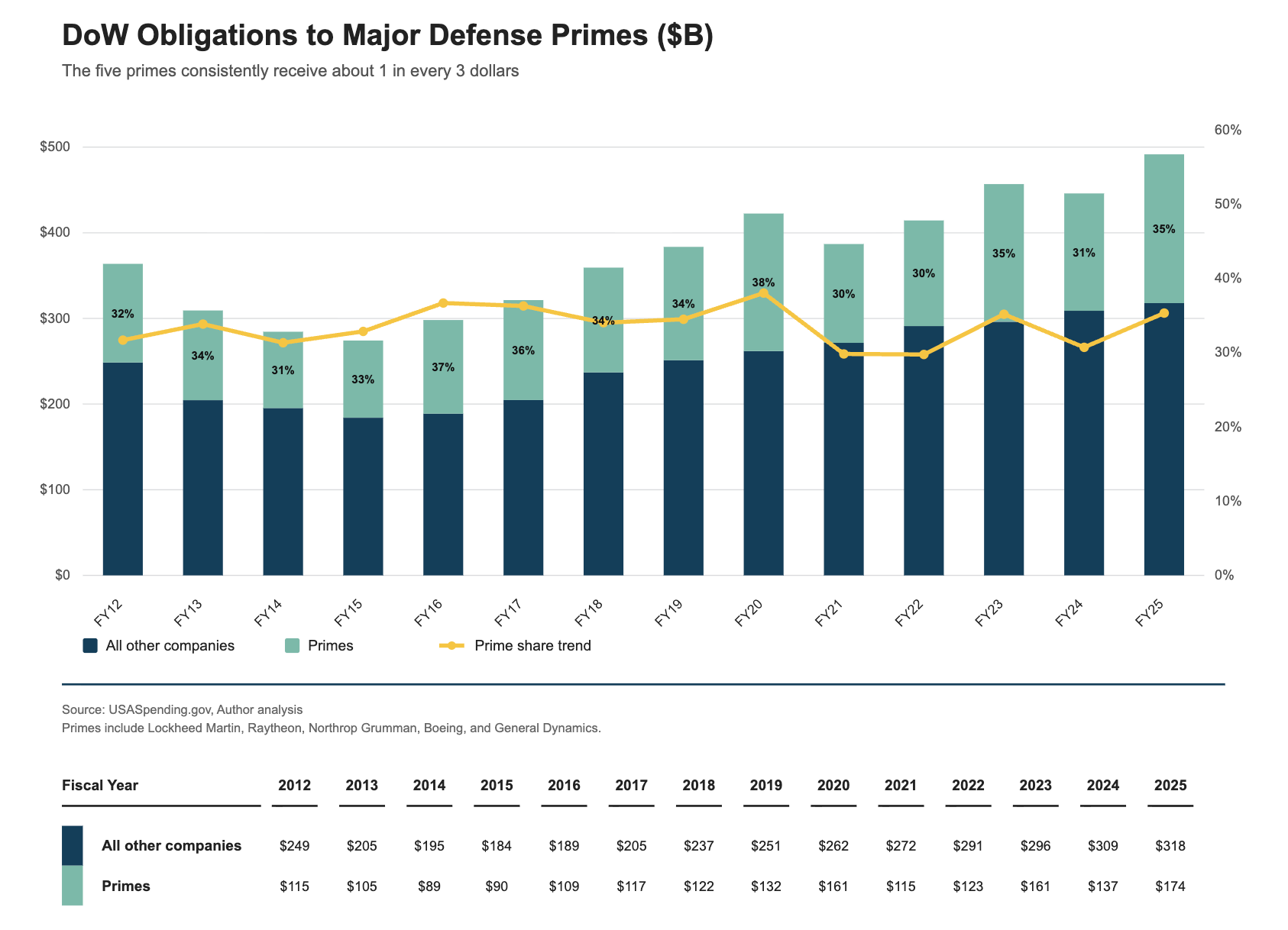

Next, I looked at the share of spending that goes to the five prime contractors. Consistently, those companies receive one in every three dollars spent by the Department. Power law outcomes in defense contracting—and many other industries—are to be expected. During World War II, the top five contractors received 20 percent of awards. However, when there is obvious discontent about the speed at which critical new systems are delivered, it’s natural to question if continued concentration among the same set of companies has contributed to stagnation.

While programs like Collaborative Combat Aircraft and the Pentagon’s newly announced purchase of 10,000 cruise missiles make it appear like dollars are diversifying, the data does not support this conclusion. A huge portion of the defense budget remains highly concentrated among just five companies. Data to date provides little visibility into whether these legacy defense primes are increasing their use of commercial items at the sub tier level. That would be informative to understand if use of commercial technology is improving below the surface. We have seen the primes invest more into their venture capital arms and partner with startups, but it’s less clear if that is being converted into adoption of commercial capabilities.

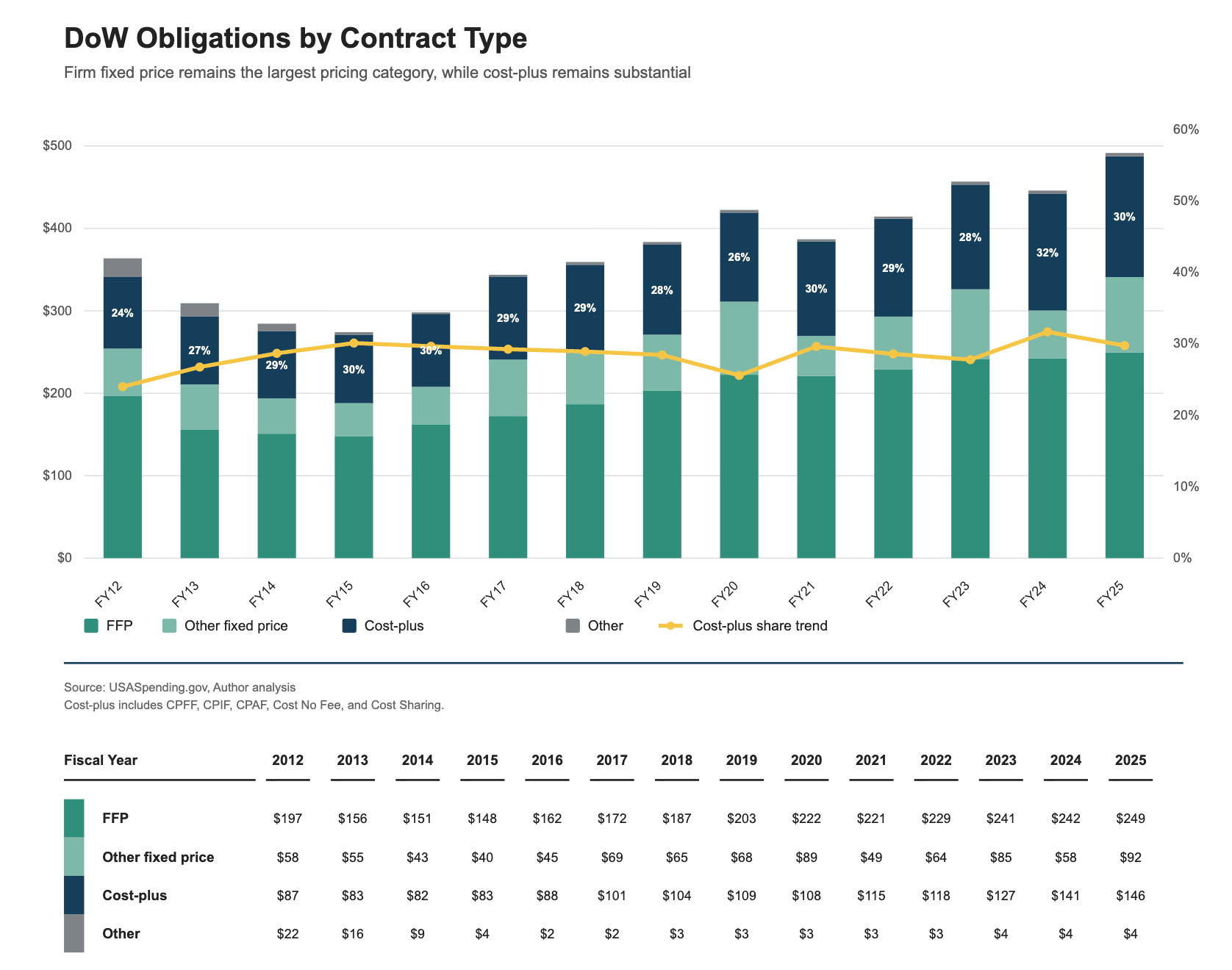

Lastly, I looked at the share of obligations by contract type. Cost-plus contracts are the vehicle of choice for about 30 percent of dollars, and the share has remained steady over time. While it’s positive that fixed-price contracts are the majority of spend, the U.S. still spent $146 billion on cost-plus contracts in FY 2025—a sum significantly greater than Germany’s annual military spend of $114 billion.

Realistic Goals for FY 2026

The acquisition system is a formidable opponent because in any given year only about 20 percent of dollars are available for new procurement starts [1]. The majority of spend is for legacy programs, such as continuation activity, renewals, maintenance, annual funding, task orders, and more. Such dollars are already spoken for, tied up in specific contract vehicles and vendors and protected from zealous reformers.

The implication is that improvements of just five percent in the metrics reviewed would require dramatic shifts in how net new dollars are spent. Retrospective analysis of FY 2025 illustrates the limited maneuver space available for reformers:

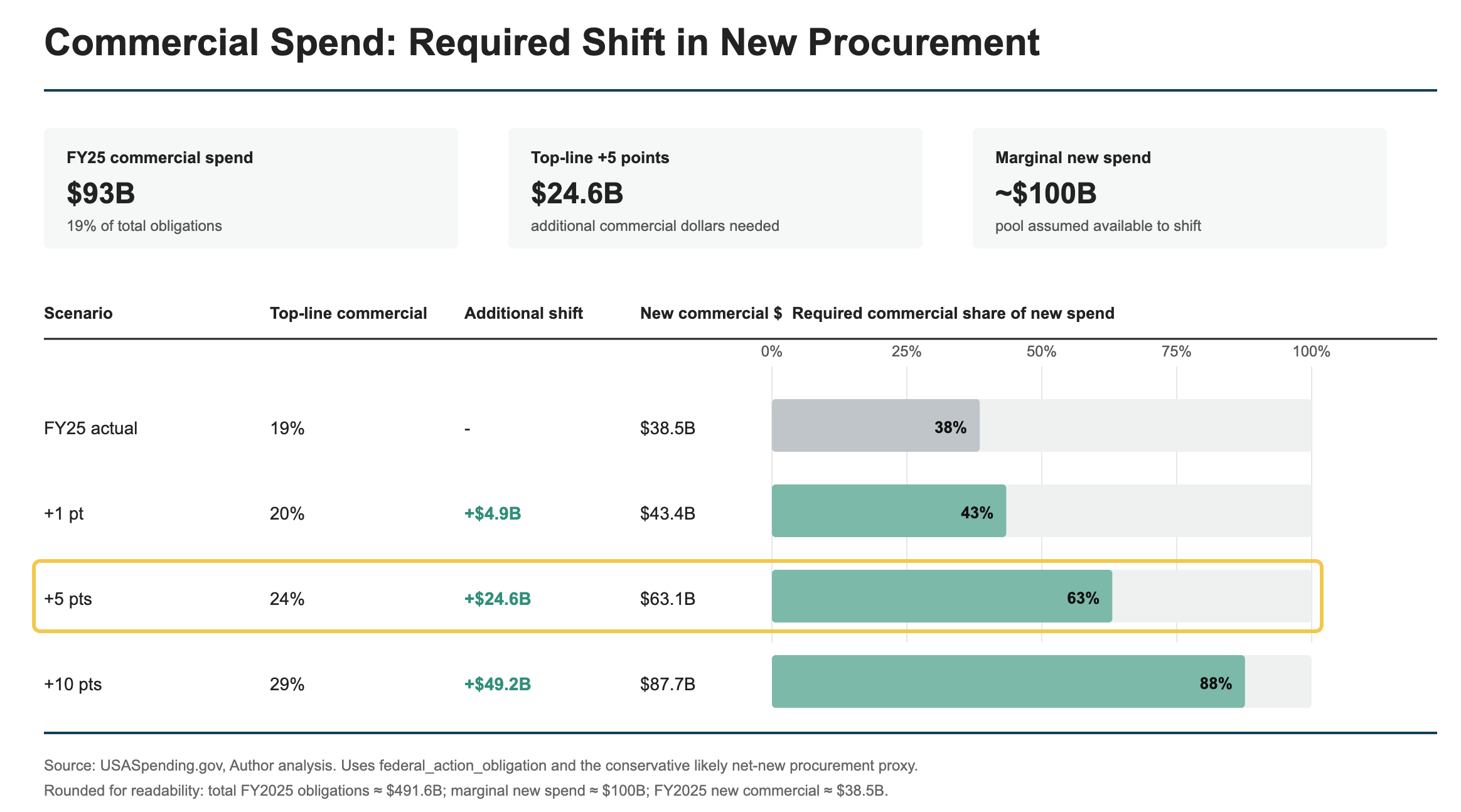

In FY 2025, commercial spend was $93 billion, or 19 percent of $490 billion. To increase the share of commercial by five points up to 24 percent would require increasing commercial spend by $24.6 billion to $117.8 billion. However, all of that change must come from the $100 billion of marginal new spend. In 2025, 38.5 percent or $38.5 billion of new spend was commercial. Shifting $24.6 billion towards commercial would require increasing net new spend on commercial up to $63 billion, which means 63 percent of all new spend would need to be commercial. This should be reasonable to expect given the aforementioned investments that NTDCs are making to provide DoW with new capability options and the increasingly innovative commercial sector.

To summarize: for the top-line obligation number to move from 19 percent to 24 percent on commercial, marginal spend on new procurement would need to be 63 percent commercial and require a shift of an additional $24.6 billion. A similar analysis for NTDCs reveals that 74 percent of new spend would need to go towards NTDCs to increase the top-line by 5 percent to 29 percent.

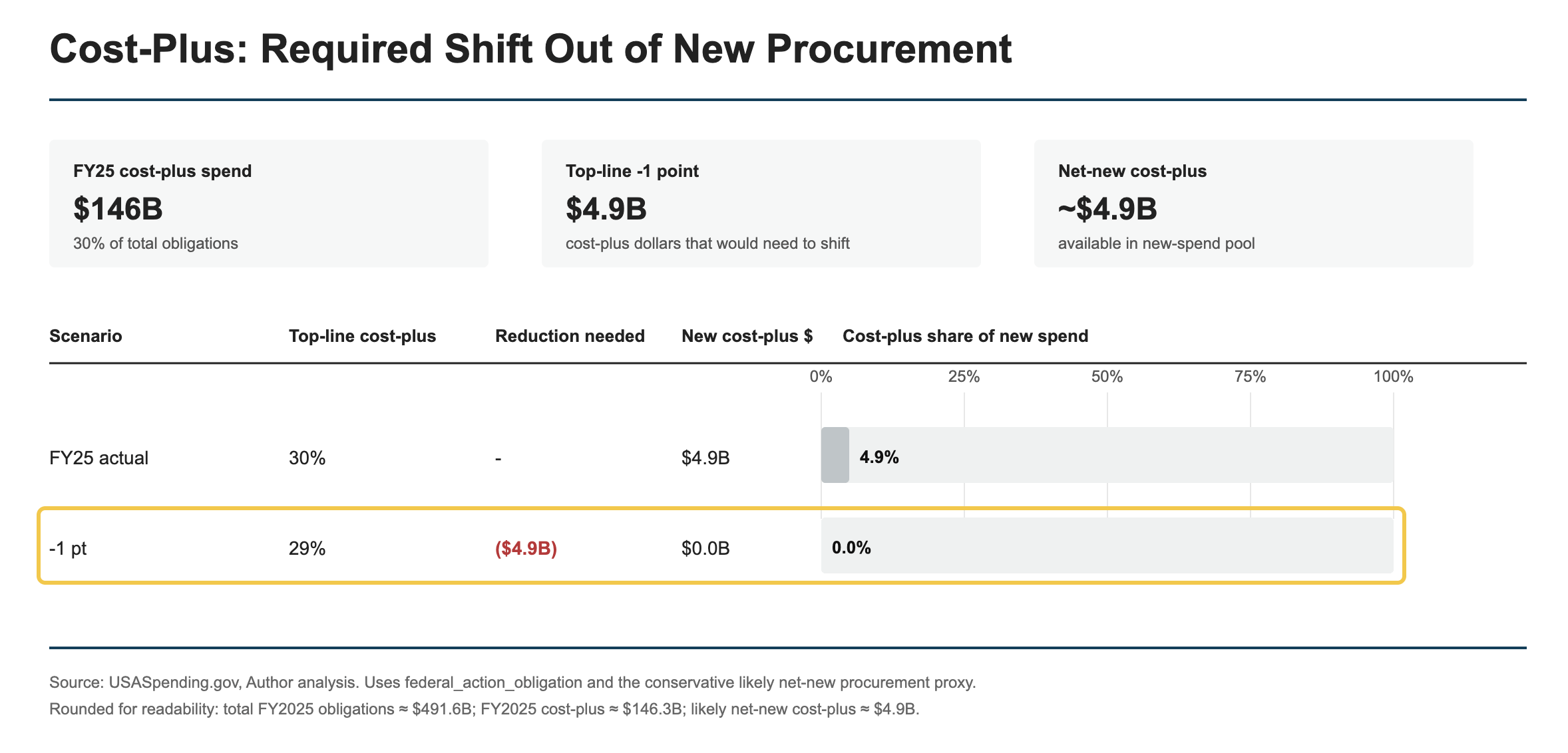

Moving the needle on cost-plus is even more challenging. In FY 2025, 95 percent of new dollars were fixed-price contracts. Only $5 billion, or 5 percent, of new spend was cost-plus. All $5 billion would need to switch to fixed price to decrease the top-line cost-plus number by just one percent, from 30 percent to 29 percent. It would be impossible to move the cost-plus number by more than one percent without cancelling or overhauling legacy programs. While it’s encouraging that new dollars are overwhelmingly fixed price, the fact that bigger changes are not possible in a given year illustrates the challenges of a large legacy portfolio.

When FY 2026 is over and the contract data is available, changes on the order of one to five percentage points for the four metrics analyzed would be a real sign of progress.

Rage Against the Machine

Even modest shifts towards commercial technology will require radical action and real accountability. FOIA’d data from Executive Order 14271 on commercial acquisition shows what reformers are up against. Of the active procurements reviewed as part of the EO, 61 percent were non-commercial. Those non-commercial acquisitions were submitted for approval, where less than one percent of the submissions were denied. The machine has no ability to check itself.

The acquisition workforce has over 160,000 people. That’s about the size of the active-duty U.S. Marine Corps. Members of this shadow service are incentivized to never deviate from the status quo and to prize documentation and compliance over outcomes. The threat of audits, protests, and GAO reports hangs over the acquisition workforce like the Sword of Damocles. Meanwhile, legacy contractors face no incentive to sub-contract work to commercial companies when they can simply build custom solutions knowing they will face no consequences.

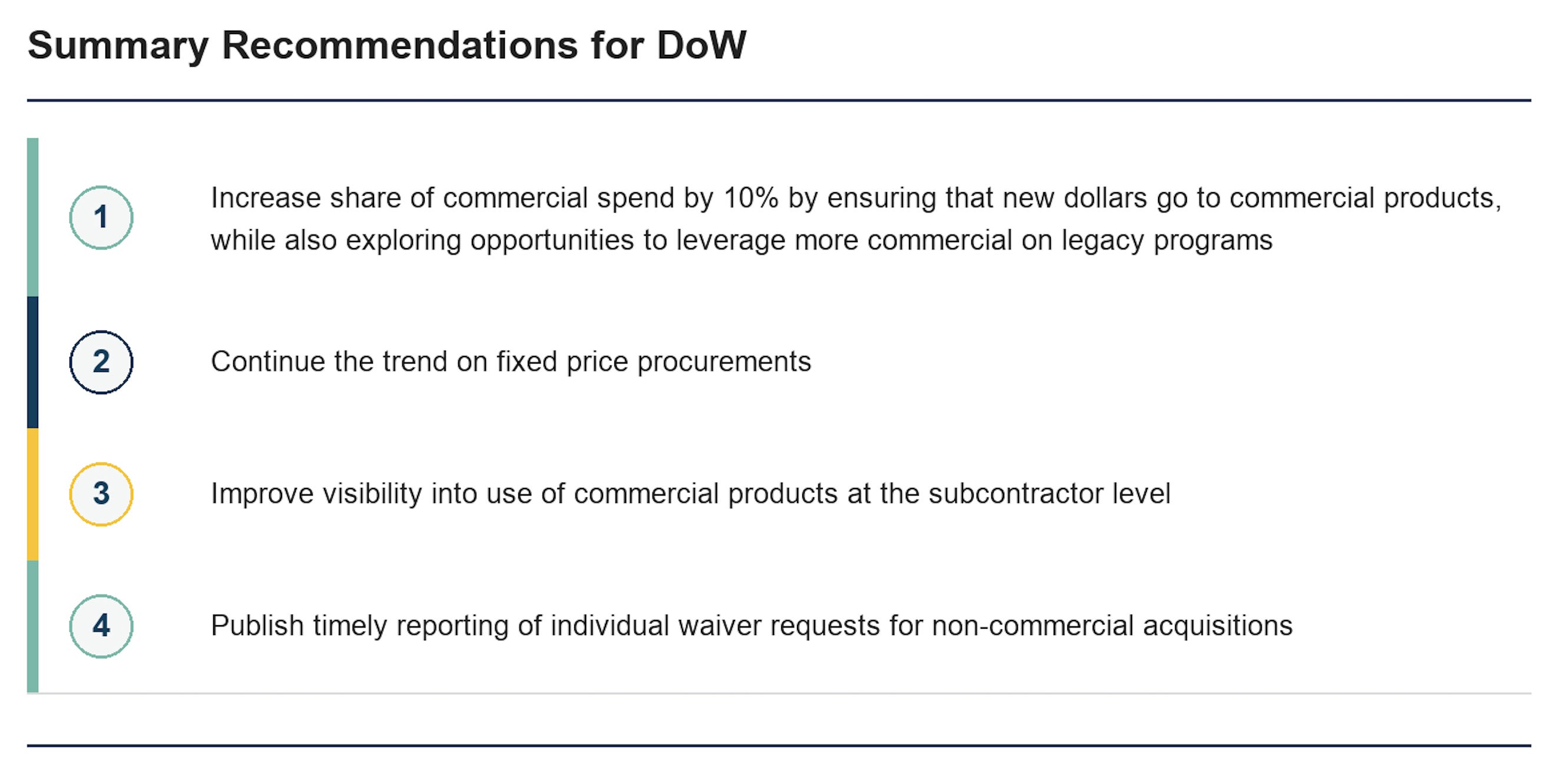

We need outsiders who will hold the system accountable. The Secretary of War should recruit an elite group of commercial leaders using existing authorities under the Federal Advisory Committee Act. This new committee of private-sector experts would review all non-commercial procurements submitted for exemption requests by contracting officers. The committee would be empowered to make recommendations to the Secretary, with a focus on where government requirements can be met with existing commercial solutions. In parallel, the DoW should staff qualified Business Operators for National Defense (BOND) agents to ensure acquisitions that should be commercial are commercial. Given the tens of thousands of acquisitions annually, an enabling technology product would be essential to scaling the operation.

Finally, contract officers should be required to publish a public notice of intent to circumvent FASA every time they pursue a non-commercial acquisition. The waiver requests could additionally be reported out in a quarterly report. This level of real-time visibility into the number of exemption requests would put positive pressure on the system.

The war in Iran is just the latest conflict to expose the fragility of the U.S. supply chain for critical weapons. America is unable to surge production because a small number of systems are made by an even smaller number of firms. We do not need more evidence that the current method of procurement is a failure mode for the long-term security of America. Rapid efforts to create a commercial industrial base will undoubtedly be painful. They should also be a national imperative.

[1] There is not an official “new start” classification in the federal obligation data. I used the following methodology on USASpend.gov data to approximate genuine new starts: Begin with base contract actions in the fiscal year, defined as transactions with modification_number = 0 for definitive contracts, purchase orders, delivery orders, and BPA calls. Then, apply a conservative keyword screen to exclude transactions with descriptors like continuation, sustainment, or renewal activity, including terms associated with sustainment, support, maintenance, repair, renewals, options, extensions, bridges, or follow-on activity. This approach is intended to avoid overcounting net-new procurement. It is not an official new-start classification and may exclude some genuinely new purchases that use continuation-style contract language. I therefore treat the resulting estimate as a conservative proxy for likely net-new procurement candidates.

Madeline Hart works Defense at Palantir and is co-author of the book MOBILIZE: How to Reboot the American Industrial Base and Stop WWIII and First Breakfast.

Join over 16,000 defense and industry subscribers to get our weekly recaps and thought pieces. Paid subscribers also get budget and legislative analysis and are valued supporters of our work.

| A guest post by

|

Awesome guest piece. Sucker for good charts.

The score depends on which layer you measure. Top-line award totals move slowly, but the interesting signal for reform is usually in the line-item and delivery-order detail — how many new entrants actually win, how obligations shift toward flexible vehicles. That granularity exists in USAspending if you're willing to dig past the summary numbers, and it often tells a different story than the headline. Would love your opinion

John